California’s Smallest Crush in 20 Years: What the 2025 Harvest Tells Us

Why down again? Demand remains soft (global consumption slump), bulk inventories are high, and vineyard removals/abandonment continue—so growers are aiming smaller to restore balance.

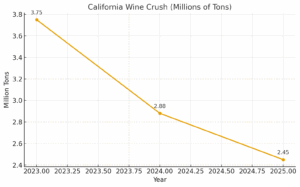

Projected crush: Under 2.5 million tons (lowest since 2004).

Year-over-year change: Down ~13% from 2024 (2.88M tons), and ~33–35% below 2023.

Unpicked fruit: Estimated 100,000–400,000 tons left on the vine again this year, reflecting weak demand and excess bulk wine.

Drivers: Soft demand, oversupply, vineyard removals, and intentional downsizing by growers to balance the market.

Regional notes: Cabernet Sauvignon and Monterey Chardonnay/Pinot show particularly steep declines.

Global Outlook – 2024 was the lowest global wine production in 60+ years, shaping cautious 2025 expectations.

Europe

France: 37.4 million hl, up 3% vs 2024 but ~13% below 5-year average. 20,000 ha uprooted since 2024 in Bordeaux. Hot, dry August reduced juice yields.

Spain: ~37–38 million hl, slightly above 2024 but still under the ~43 million hl 10-year average

Italy: Rebounding to ~45–47 million hl, near the 5-year norm, though Tuscany and some regions remain down.

Southern Hemisphere

Australia: Modest rebound after several short vintages; earlier harvest due to heat and dryness.

Argentina: Recovering yields but variable quality.

Chile: Still trailing expectations, with weather-related challenges.

Summary: 2025 continues the trend of historically low wine harvests. California is facing its smallest crush in two decades, with significant fruit left unpicked. Globally, Europe is mixed—Italy steady, France and Spain below average—while the Southern Hemisphere shows modest recovery. The overarching theme is purposeful contraction to bring supply back in line with shrinking demand.